Chitra, now a married 35-year-old woman living in Delhi with a 3-year-old child, earned Rs 30,000 per month in 2013. Back then, as a single woman with fewer financial responsibilities, this amount comfortably covered her expenses, including rent, groceries, transportation, and some leisure activities. Fast forward to 2024, and Chitra’s income has risen to Rs 50,000 per month. On the surface, this seems like a substantial raise, almost a 67% increase. However, due to inflation, the reality is quite different.

The impact of inflation

In 2013, Rs 30,000 had a certain purchasing power, allowing Chitra to buy a specific amount of goods and services. Inflation, which is the increase in prices of goods and services over time, has eroded that purchasing power.

To understand this better, let’s use the Cost Inflation Index (CII) provided. In 2013, the CII was 200, and in 2024, it is 363.

Here’s how Chitra’s 2013 income translates to today’s terms:

Income in 2013: Rs 30,000

The CII for 2024: 363

The CII for 2013: 200

The ratio is 363 divided by 200, which equals 1.815

Multiply Rs 30,000 by 1.815 to get Rs 54,450

So, Chitra’s Rs 30,000 in 2013 is equivalent to Rs 54,450 in 2024. Despite her raise to Rs 50,000, Chitra’s income has not kept pace with inflation. In real terms, her current salary has less purchasing power than her salary in 2013.

Inflation’s real impact

Every Re 1 earned in 2013 is now effectively worth Re 0.55 in 2024. This means that Rs 30,000 from 2013, adjusted for inflation, would need to be approximately Rs 54,450 to maintain the same standard of living. Chitra’s current income of Rs 50,000 falls short of this amount, showing that inflation has eroded her real income.

Chitra’s situation shows how inflation affects everyone’s finances. Despite nominal increases in income, the rising cost of living can result in a net loss in purchasing power, leaving individuals like Chitra feeling financially strained.

This is when citizens look to the Budget presentation in the hope of some relief. The full Budget 2024 will be presented on July 25 by Finance Minister Nirmala Sitharaman.

“Taxpayers expect higher deductions under the old regime and hope the new regime will allow more people to retain a greater portion of their income after taxes,” says Adhil Shetty, CEO of Bankbazaar.com.

Tax regimes: Old vs New

Old tax regime

The old tax regime offers various tax deductions, including loan payments, insurance premiums, tax-saving investments like the provident fund, tuition fees, and medical expenses.

“These deductions are sizeable and lower the tax liabilities for many who prefer it to the new regime where deductions are few. In the absence of inflation adjustment to the old slab rates frozen at 2013 levels, taxpayers continue to pay inflated tax rates while costs of living soar,” states Bank Bazaar’s Primer Budget 2024.

New tax regime

The new tax regime, on the surface, appears inflation-friendly. However, its positive impact is felt only on incomes up to Rs 15 lakh. Up to this level, the effective tax rates seem lower than inflation-adjusted values from 2013-14. Above the Rs 15 lakh level, there is no inflation adjustment provided by the new regime.

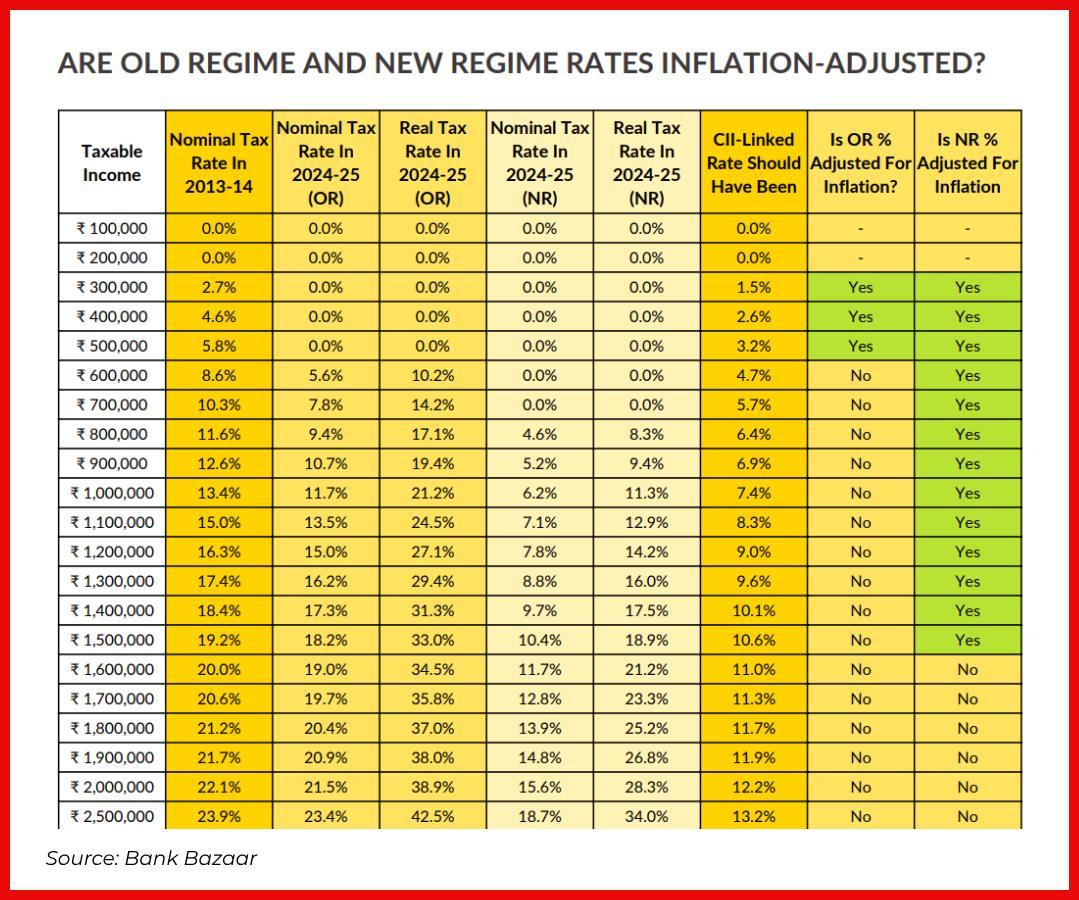

Frozen tax slabs: Unchanged since 2013-14

For instance, a taxable income of Rs 10 lakh under the old regime has a tax liability of Rs 1.17 lakh—an effective rate of 11.7%. Under the new regime, it’s Rs 62,400 or 6.24%. Adjusted for inflation, the value of Rs 10 lakh in 2013 is worth Rs 5.5 lakh in 2024, making the ‘real’ tax rate 21% in the old regime and 11.3% in the new regime. The ‘real’ rate rises as high as 55%-58% on incomes above Rs 50 lakh and under Rs 1 crore.

"tax")

Inflation adjustment issues

"tax")

Excess taxes being paid

"tax")

Budget 2024: What Bank Bazaar suggests

— The highest tax rate of 30% should be applied to income above Rs 18 lakh, and 20% on income above Rs 9 lakh.

— Taxpayers in the high-income bracket prefer the old regime with tax slabs frozen at 2013-14 levels. The report recommends updating the tax slabs.

— The 0% tax slab, currently applicable for income under Rs 2.5 lakh, has been unchanged since July 2014. The report suggests raising it to Rs 5 lakh.

— Additionally, it proposes a 5% to 10% tax on income between Rs 5 lakh and Rs 9 lakh, 20% on income between Rs 9 lakh and Rs 18 lakh, and 30% on income above Rs 18 lakh.

The report calls for several enhancements in deductions:

1. 80C limit: Increase the deduction limit under 80C to at least Rs 2 lakh from the current Rs 1.5 lakh, which was set in 2014.

2. 80D deductions: Enhance 80D deductions to Rs 50,000 for general taxpayers and Rs 1 lakh for senior citizens, considering the rising costs of insurance premiums post-pandemic.

3. Home loan interest and principal payments: These should be in a separate section and increased to Rs 5 lakh.

4. 87A rebates: Extend rebates under 87A to incomes up to Rs 6.3 lakh, benchmarking the last update done in 2019.

What New India needs: A regulatory Budget 2024 wishlist:

1. Continue facilitating paperless, presence-less access to credit through initiatives like Video KYC, enhancing fintech innovation and customer convenience.

2. Recognise fintech’s strategic role

3. Persist with efforts like India Stack, fostering a digital revolution in credit access and bolstering economic growth.

4. Strengthen collaboration platforms between banks and compliant FinTech companies

5. Sustain support for FinTech and MSME start-ups with tax reliefs and policy frameworks that nurture innovation and attract investors.

What the Finance Ministry should continue doing, according to the report:

1. RBI regulations should promote and ease partnerships between banks and FinTechs, fostering financial innovation and inclusion.

2. Improve DigiLocker integration with income tax and provident fund services for seamless financial document management.

3. Allocate 25% of the “Anusandhan” Rs 1 trillion fund to fintech innovation

4. Incorporate comprehensive personal finance education into primary and secondary school curriculums to build a financially

literate society.

5. Align long-term capital gains taxation for unlisted equities with listed ones to bolster investment in the FinTech industry.

Shetty says, “Since the majority of taxpayers prefer the old regime despite the lack of inflation adjustment, higher tax exemptions need to be provided in the new regime. This would make the new regime much more attractive.”